Corda Protocol for Central Bank Digital Currency

Central Bank Digital Currency gains interest across the Globe.

Central Banks are conducting research and embarking on Proof Of Concept.

Let’s have a brief look at wholesale and retail CBDC and benefits of its blockchain-alike implementations.

Fin-Techs Without Banks

With CBDC, fintechs will be able to provide services without banks.

TODAY: Any fintech provides new services on top of the existing banking infrastructure.

Retail Central Bank Digital Currency (CBDC) opens opportunities to extend access to digital central bank money =>

TOMORROW: fintechs will be able to provide services without banks.

Wholesale vs Retail CBDC

| Criteria | Wholesale CBDC | Retail CBDC |

|---|---|---|

| Audience | Limited to commercial banks, clearing institutions and other entities that traditionally have access to Central Bank (CB) reserves | Has a larger user base, can involve corporates, small businesses and individuals. Refers to those who currently do not have access to central bank money |

| Technology lvl | Last step in Real Time Gross Settlement (RTGS) technical solutions evolution, which has 50-year history and is been modernized every few decades | Young from tech point, currently does not exist in production. However, CBs across the world are beginning to commit resources towards implementing it |

| Projects | Atomic Delivery: Bank of Canada: Project Jasper Phase 3 | Proposed projects\: |

| ^^ | Cross-border payments: Bank of Thailand: Project Inthanon Phase3 | ^^ - Within single currency zone |

| ^^ | Efficient complex payments workflows: Project Urbin - blockchain improves core features of RTGS systems: reducing gridlock, enhancing flexibility, giving more control and real time visibility of payments netting network-wide to banks | ^^ - BC-based CBDC solution |

Proposed Retail CBDC Projects

Within single currency zone

Private sector payments innovation focuses on the front end system - which faces users directly, including new ways of payment initiating (mobile/contactless) and overlay systems which wrap existing settlement systems and most of an existing framework around fresh interfaces.

Over the past decade, we see increasing number of nations have implemented faster or real-time payments systems:

- UK: Faster payments

- India: IMPS

- Australia: NPP

- Russia: Quick Payments System

- total: 54 countries

- +14 countries in 2019

Yet these solutions provide new digital rails for payments within a currency zone, services are offered via consumer’s bank accounts, and txs are settled inter-bank.

Worth mentioning here, WeChat and Alipay in China. These are full-stack but closed-loop payments systems: both payer and payee live in the same system, no settlement across separate systems takes place. It cannot be a global solution because of: coordination challenge, risk concentration which comes as the cost of a lack of interoperability.

Blockchain-based CBDC solution

Cryptocurrency concept with stable coins looks more promising here.

- distributed custody and p2p transfers,

- integration with a larger Ecosystem,

- improved security and resilience by removing honey pots of data and centralized weak points

All these features are natural attributes of blockchain-based systems.

This represents the paradigm shift from account-based transfer of value to storing and transferring of value on blockchain.

Blockchain enables:

- the digital storage and transfer of value,

- Interoperability between different asset types,

- global integrity of the system in which CBDC exists,

- security improvement over centralized payments systems.

While some (public) blockchains have known drawbacks:

- Data privacy,

- Identity,

- Scalability,

- Probabilistic settlement.

According to R3 consortium, Corda blockchain protocol overcomes all of them:

- built on requirements for regulated enterprises,

- creates environment that adheres to regulatory standards,

- has unique p2p design: data is only shared with relevant parties,

- identity present by default beginning as it’s a private chain,

- scalability enhanced with uncoupled tx run in parallel and p2p data distribution techniques,

- settlement finality guaranteed by Corda’s consensus model.

To prove this in action, R3 conducted an experiment with DLT for domestic network together with the Bank of Canada: Project Jasper. Among its conclusions, it was found that DLTs alowing integration with financial market infrastructure ecosystem along with settlement finality, privacy and scalability, such as Corda, could run it better than existing proof-of-work blockchains like Ethereum, still being more cost-effective.

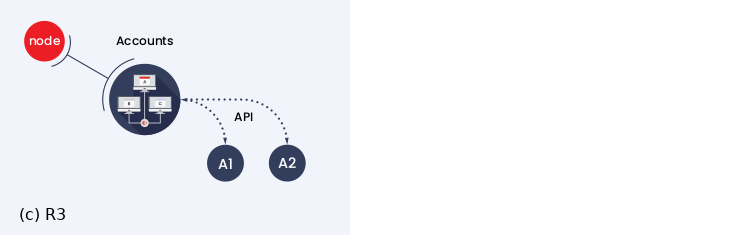

API implementation for BC-based CBDC

For those who won’t, the mechanism of API accounts comes into play.

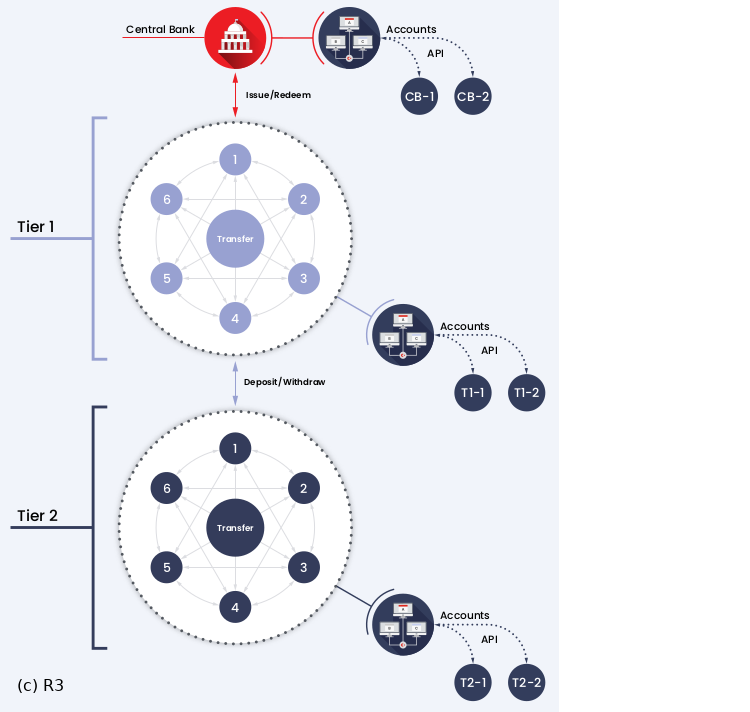

It is described in the generalized implementation option for CBDC proposed by R3. A user will communicate with a chain node through an API:

A node can be held by organizations of two tiers:

-

Tier-1: privileged wholesale financial institutions that can interact with central bank and hold and transfer tokens themselves.

-

Tier-2: retail users (fintechs), that can interact with tier-1 and transfer tokens between themselves.

Top-level structure scheme of account-based CBDC looks like this one:

-

Central Bank Digital Currency: an innovation in payments, white paper by R3 ↩︎